February 16, 2025

Data from the National Energy Administration showed that investment in power grid projects exceeded 608.3 billion yuan in 2024, up 15.2% YoY, marking a record high in recent years. With the State Grid's investment scale in 2025 targeting a historical peak of 650 billion yuan, the ultra-high voltage (UHV) sector is becoming the main battlefield for investment. Notably, against the backdrop of an overall positive industry trend, aluminum wire and cable enterprises are undergoing structural adjustments—despite the YoY contraction in UHV conductor and ground wire tender volumes in 2024, which pressured post-holiday operations, the State Grid released over 200,000 mt of aluminum wire and cable orders at the beginning of 2025. Among these, UHV projects accounted for 130,000 mt, while transmission and transformation projects contributed 80,000 mt of core orders, injecting a strong boost into the industry chain.

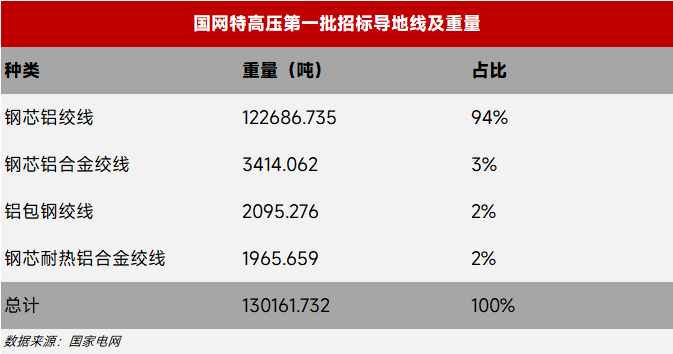

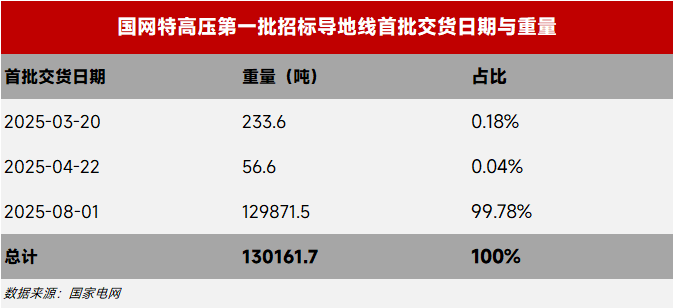

Focusing on the first batch of UHV tenders in 2025, the 130,000 mt conductor and ground wire orders dominated by the Gansu~Zhejiang ±800kV and Phase IV of the Pingwei Power Plant projects featured JL1/GA steel-core aluminum stranded wires with conductivity ≥61.5% IACS as the most-traded type, which is expected to significantly boost market demand for high-conductivity aluminum rods (L1). Regarding the delivery schedule, the staggered delivery starting in August will continue until Q1 2026, providing medium and long-term capacity support. In contrast, the 73,000 mt JL3/GA orders (conductivity ≥62.5% IACS) for transmission and transformation projects, with a concentrated delivery window from May to June, will drive production stockpiling in April, becoming a key driver for the rebound in Q2 operating rates.

SMM believes that the current order structure is reshaping the industry cycle: the short-cycle quick delivery (April stockpiling/May-June delivery) of transmission and transformation projects and the long-cycle stable demand (continuous release starting in August) of UHV projects form a momentum relay. Considering that the State Grid's tenders started 2-3 months earlier than in previous years, a new round of order releases is expected by the end of Q2. Coupled with the implementation of the 650 billion yuan annual investment target, the aluminum wire and cable industry is likely to emerge from the "order gap period" and achieve a systematic rebound in capacity utilization rates in H2.